Outsourced Bookkeeping Services | FSMC Bookkeeping Services

September 3, 2025

Cross Border Tax Planning Topics to Consider

October 4, 2025

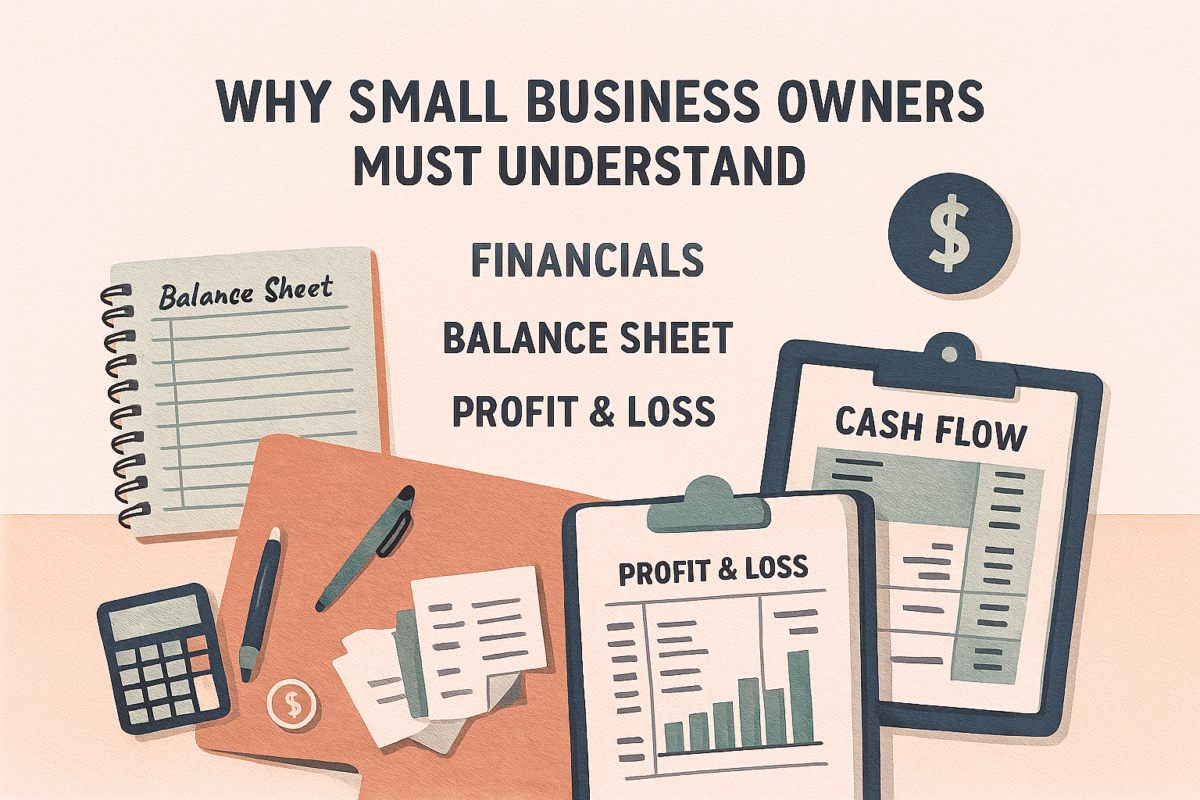

Why Small Business Owners Must Understand Financials

by: FSMC Bookkeeping Services

Introduction

Running a small business means wearing many hats—salesperson, manager, marketer, and sometimes even bookkeeper. While it’s tempting to delegate financials or only think about them at tax time, understanding your financial statements is essential for survival and growth.

Your balance sheet, profit and loss statement (P&L), and cash flow statement aren’t just accounting paperwork. They’re powerful tools that reveal how healthy your business is, where money is going, and how you can make smarter decisions.

In this article, we’ll break down these three key reports, explain how they’re used, highlight common mistakes business owners make, and show why hiring a professional bookkeeper can save you time and money.

The Balance Sheet

What Is a Balance Sheet?

The balance sheet is a snapshot of your company’s financial health at a single point in time. It shows three major categories:

- Assets – everything your business owns (cash, accounts receivable, inventory, property, equipment).

- Liabilities – everything your business owes (loans, accounts payable, credit card balances, taxes).

- Equity – the owner’s investment and retained earnings (essentially, what the business is worth after debts).

How a Balance Sheet Is Used

Lenders, investors, and owners use the balance sheet to understand financial stability. It answers questions like:

- Do I have enough cash to cover debts?

- How much is my business worth?

- Am I over-leveraged with loans?

Why the Balance Sheet Is Important

Without it, you might believe you’re in good shape when in reality, your assets could be tied up in receivables while short-term bills pile up. It’s your financial scorecard at any given moment.

Common Balance Sheet Mistakes

- Overvaluing receivables: Counting money that may never come in.

- Overlooking liabilities: Forgetting short-term obligations like taxes or vendor bills.

- Treating it as a formality: Using it only for banks instead of as a decision-making tool.

The Profit and Loss Statement (P&L)

What Is a P&L Statement?

Also called an income statement, the P&L shows your revenue, expenses, and profit (or loss) over a given period—usually monthly, quarterly, or annually.

How It’s Used

The P&L helps business owners:

- See whether they’re making or losing money.

- Identify which products or services are most profitable.

- Track expenses that may be creeping up.

Why the P&L Is Important

Your P&L provides a roadmap for growth. By reviewing it regularly, you can:

- Spot trends (rising costs, seasonal revenue shifts).

- Adjust pricing strategies.

- Reinvest profits strategically.

Common P&L Mistakes

- Mixing personal and business expenses: This muddies the waters and inflates costs.

- Misclassifying expenses: Poor categorization makes analysis impossible.

- Looking only once a year: Waiting until tax time prevents proactive adjustments.

The Cash Flow Statement

What Is Cash Flow?

The cash flow statement tracks how much money actually comes in and goes out of your business. Unlike the P&L, which shows income whether or not it’s collected, cash flow shows real deposits and payments.

How Cash Flow Is Used

Cash flow reveals:

- If you can cover payroll and bills.

- How quickly customers are paying invoices.

- Whether you need financing to handle gaps.

Why Cash Flow Is Critical

Many profitable businesses fail simply because they run out of cash. Understanding your cash flow ensures you can:

- Survive seasonal slowdowns.

- Negotiate payment terms with vendors.

- Avoid emergencies where expenses exceed available funds.

Common Cash Flow Mistakes

- Confusing profit with liquidity: You can be profitable on paper and broke in reality.

- Ignoring unpaid invoices: Counting money that hasn’t arrived.

- Not planning ahead: Forgetting upcoming obligations like quarterly taxes or loan payments.

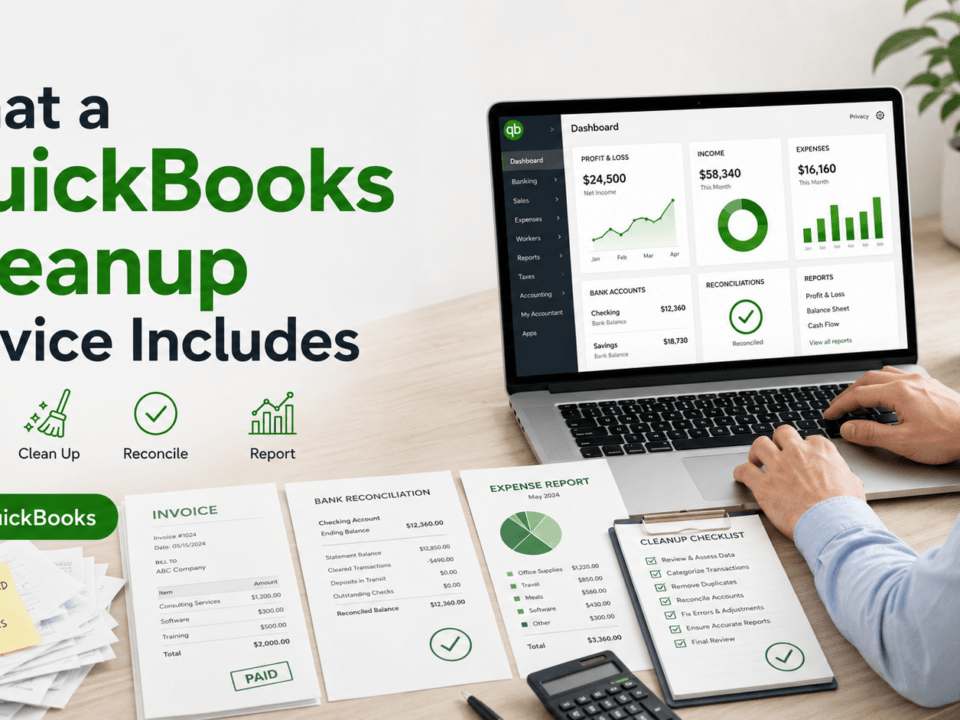

Why Hiring a Professional Bookkeeper Matters

Time Savings for Business Owners

Bookkeeping is time-consuming. A professional can save you hours each week, allowing you to focus on what actually grows your business—sales, customer relationships, and innovation.

Accuracy and Compliance

A bookkeeper ensures your records are accurate, reconciled, and tax-ready. That means fewer mistakes, less stress at tax time, and a reduced risk of costly penalties.

Better Decision-Making With Clean Data

When your books are up-to-date, you have clear insights to make strategic decisions. Can you afford to hire another employee? Should you expand operations? You’ll know the answer with confidence.

Financial Savings and ROI

Hiring a bookkeeper pays for itself by:

- Preventing overpayment of taxes.

- Avoiding late fees and penalties.

- Identifying opportunities for cost savings.

Focus on Growth Instead of Paperwork

Most importantly, outsourcing your bookkeeping gives you freedom. Instead of spending evenings buried in spreadsheets, you can focus on clients, revenue, and scaling your business.

Conclusion

Your balance sheet, profit and loss statement, and cash flow report are more than financial documents. They’re the compass of your business, showing you where you stand and where you’re headed.

While it’s crucial to understand these reports, maintaining them can be overwhelming. That’s where professional bookkeeping makes all the difference. You save time, reduce errors, and gain clarity—so you can focus on what truly matters: growing your business.

👉 Take the stress out of your finances with FSMC Bookkeeping Services.

Reach out to learn more at: Contact Us

#SmallBusiness #Bookkeeping #CashFlow #ProfitAndLoss #BalanceSheet #BusinessGrowth

{kind=link}

{kind=link}

{kind=link}