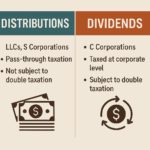

Understanding How Dividends and Distributions Are Taxed

July 3, 2025

Seasonal Jobs and Taxes

July 3, 2025

What Banks Won’t Tell You About Credit Cards

Compliments of FSMC Bookkeeping Services

Credit cards can be powerful tools for building credit and managing expenses — but they’re also packed with features and policies that many banks don’t fully explain. While the surface looks shiny with perks and points, the fine print often tells a different story. Here’s what you need to know before swiping that card again.

1. Minimum Payments Are a Costly Trap

Minimum payments seem manageable — usually just 2% to 3% of your total balance — but paying only that small amount allows interest to accumulate quickly. Over time, this means you could pay double or even triple the original cost of a purchase. To avoid unnecessary interest, aim to pay your balance in full every month.

2. You Can Negotiate Your Interest Rate

Most people don’t realize that credit card interest rates aren’t set in stone. If you’ve been a dependable customer — consistently paying on time — there’s a good chance your credit card issuer will lower your APR if you simply ask. A short call to customer service could save you hundreds of dollars over the long term. Banks would rather retain a loyal customer than lose you to a competitor.

3. Rewards Programs Are Not Always Rewarding

Cash back, miles, and points sound appealing, but many of these programs come with hidden costs. High annual fees and increased spending temptations can lead you to carry a balance — and that’s where the banks profit. The best way to benefit from rewards is to only use your card for planned expenses and to pay it off in full each month. That way, you enjoy the perks without the penalty.

4. Late Fees May Be Waived — If You Ask

Missed your due date? Don’t panic. Most credit card companies offer a grace period for late payments, and they’re often willing to waive the late fee if it’s your first offense. But you must call and ask. Banks don’t promote this option because late fees generate a significant amount of revenue.

5. Introductory Offers Come with Conditions

0% APR offers and bonus rewards look attractive, but they often come with fine print. Some require you to spend a certain amount in the first few months or maintain a perfect payment history to retain the benefit. If you miss a payment or don’t meet the spending threshold, you could lose the perk or even face retroactive interest. Always read the full terms before applying for any promotional offer.

6. Your Spending Behavior Is Being Watched

Banks analyze your spending habits to tailor offers and promotions. If you’re someone who pays off their balance every month, you might get fewer rewards-based offers because you’re not as profitable. However, those who frequently carry a balance are more likely to receive credit line increases or cross-sells for additional financial products. Being aware of how your behavior influences what you’re offered can help you make smarter decisions.

Smart Credit Card Use: Take Back Control

Credit cards don’t have to be a trap. When used strategically, they can help you build credit, earn rewards, and manage cash flow. The key is to understand how the system works — and where it works against you.

Here are some tips to stay in control:

✅ Pay your full balance every month

✅ Monitor your spending

✅ Don’t chase rewards unless it makes financial sense

✅ Ask for interest rate reductions

✅ Always read the fine print

At FSMC Bookkeeping Services, we help individuals and businesses make sense of their finances — including how credit card use can affect your cash flow, taxes, and long-term planning. Whether you need help managing expenses, preparing for tax season, or improving your bookkeeping systems, we’re here to help across the USA and Mexico.

Let’s take control of your finances, together. Contact us today: